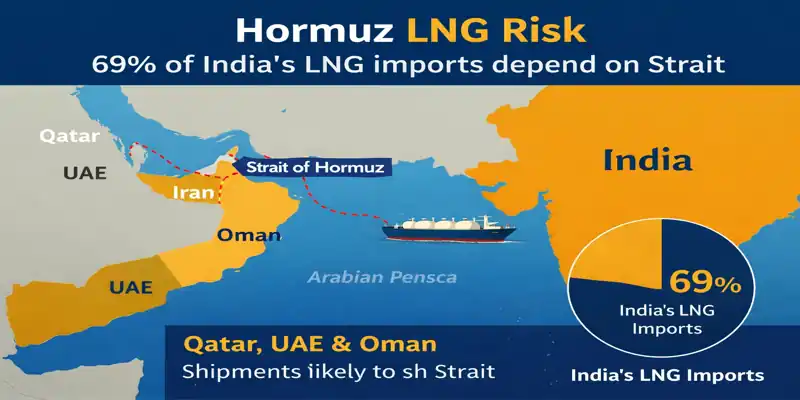

The Strait of Hormuz LNG supply risk is emerging as a major concern for India’s energy security. A new report by Elara Securities warns that nearly 69% of India’s liquefied natural gas (LNG) imports depend on shipments passing through the Strait of Hormuz.

This narrow shipping corridor connects the Persian Gulf with global energy markets. Any disruption in this region could affect LNG supply to India and other major importing countries.

The report titled “LNG: Steering through the Hormuz bottleneck” highlights the vulnerability of India’s LNG supply chain due to heavy dependence on Middle Eastern suppliers.

Hormuz LNG Risk for India’s Gas Supply

According to the report, by calendar year 2025, India is expected to import around 17.5 million tonnes of LNG from Qatar, the UAE, and Oman.

This volume equals roughly 63 million standard cubic metres per day (mmscmd) of natural gas.

Most of these LNG shipments travel through or close to the Strait of Hormuz, making India’s LNG supply highly exposed to geopolitical or shipping disruptions in the region.

Even after adjustments through LNG swap arrangements, the exposure remains significant.

The report states that GAIL’s LNG swap optimisation with US supplies slightly reduces the risk. However, the effective exposure still remains around 66%, which indicates a high concentration of supply dependence.

India LNG Imports Depend on Strait of Hormuz

India’s LNG import terminals also face varying levels of exposure to supply disruptions linked to the Strait of Hormuz LNG supply risk.

The report identifies Petronet LNG’s Dahej terminal as the most vulnerable facility. This terminal handles the largest share of LNG imports in India.

About 76% of Dahej’s LNG supply is connected to shipments originating from or passing through the Strait of Hormuz.

Other LNG terminals also show significant dependency on Middle Eastern supply routes.

-

Mundra LNG terminal: 88% exposure

-

Dhamra LNG terminal: 65% exposure

-

Ennore LNG terminal: 62% exposure

The Kochi LNG terminal and Chhara LNG terminal are fully dependent on LNG supplies from the Middle East. However, these facilities currently operate at relatively smaller volumes compared to Dahej.

This high dependence highlights the importance of diversifying LNG supply sources and strengthening energy security.

Impact on LNG Companies and Gas Infrastructure

The Strait of Hormuz LNG supply risk could also affect major gas companies and transmission networks in India.

The report identifies Petronet LNG and Gujarat State Petronet Limited (GSPL) as companies with the highest exposure.

Petronet LNG has around 77% exposure to LNG shipments linked to the Strait of Hormuz. This heavy dependence directly affects the company’s regasification revenue.

Meanwhile, 62% of GSPL’s gas transmission volumes depend on LNG sourced through this critical shipping route.

If LNG shipments are disrupted, the impact could spread across the entire gas value chain.

According to the report, the earnings impact would likely move sequentially across the sector. The disruption would first affect terminal utilisation, followed by pipeline transmission throughput, and eventually impact industrial gas consumption margins.

Downstream Gas Consumers Also at Risk

Industrial gas consumers may also face supply constraints if LNG shipments are disrupted.

The report notes that Gujarat Gas is particularly vulnerable. Around 73% of its gas supply comes from LNG imports.

Due to constrained regasified LNG availability, Gujarat Gas has already issued force majeure notices to industrial customers. The company started curtailing gas supply to industries from March 6.

However, some companies remain relatively less exposed to the Strait of Hormuz LNG supply risk.

For example, GAIL India’s marketing segment has only 16% dependence on Gulf LNG supply. The company has diversified supply contracts with producers in the United States, Russia, and Australia.

Similarly, city gas distribution companies such as Mahanagar Gas and Indraprastha Gas are less affected. These companies rely more on domestic natural gas allocations, especially for priority sectors like CNG and household consumption.

Need for LNG Supply Diversification

The report concludes that India must diversify its LNG sourcing strategy to reduce dependence on a single shipping corridor.

Expanding supply contracts with countries outside the Gulf region and increasing domestic gas production could help reduce exposure to geopolitical risks.

With global energy markets facing rising uncertainty, the Strait of Hormuz LNG supply risk highlights the importance of building a more resilient LNG supply chain for India.